Mandatory car accident reporting requirements by state

MPH Photos // Shutterstock

When the unexpected happens on the road, knowing your legal obligations can be the difference between a minor inconvenience and a major headache. While we all hope to never be in a car accident, it’s important to be prepared. Beyond exchanging insurance information and filing a police report, many states require you to file a separate accident report directly with the state’s Department of Motor Vehicles (DMV) or an equivalent agency. This can feel confusing, but CheapInsurance.com breaks it all down.

Why Is This State-Level Report So Important?

Think of it this way: A police report is for law enforcement’s records, and an insurance claim is for your provider’s records. But a state accident report is for the government’s records. This information helps it track accident statistics, identify dangerous intersections, and ensure drivers are compliant with state laws. Filing this report correctly and on time can help you avoid fines, license suspension, and other penalties. It’s your official, verifiable account of the incident.

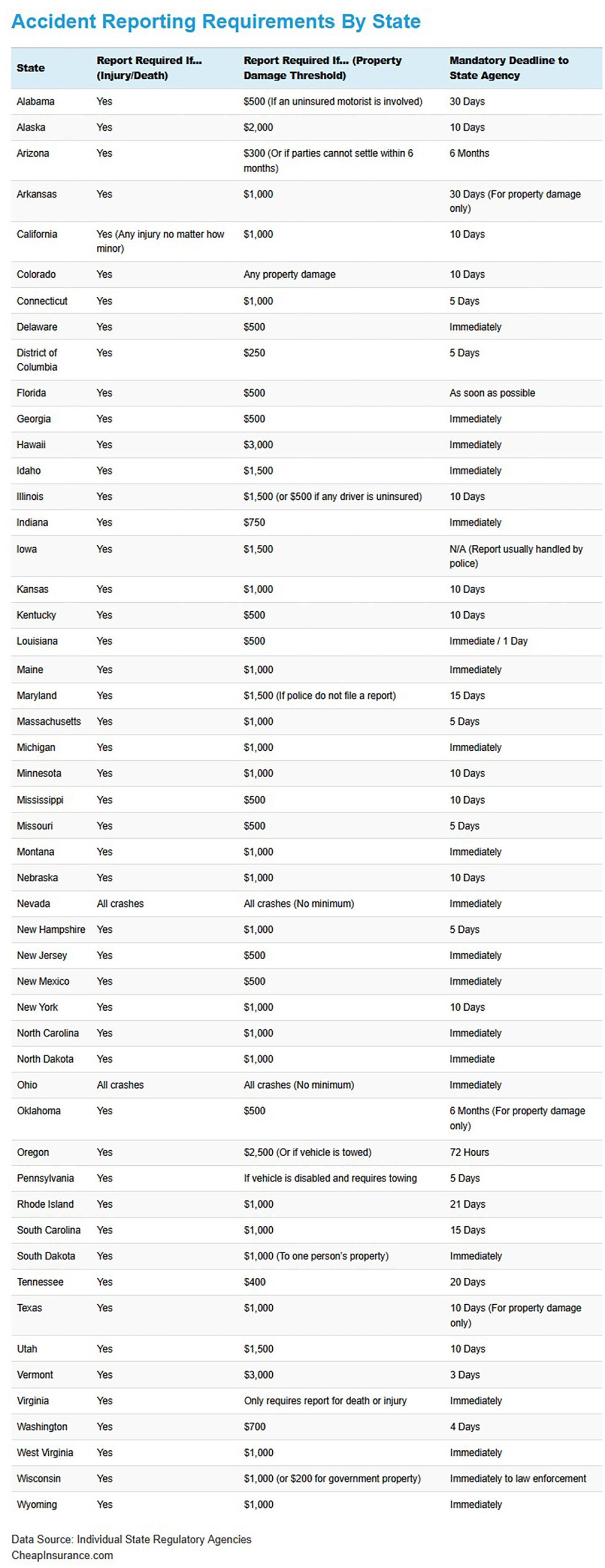

State-by-State Breakdown: What You Need to Know

The rules vary wildly from state to state, so pay close attention! We’ve put together a comprehensive table to help you navigate the tricky waters of mandatory accident reporting. The requirements usually depend on two key factors:

- Injury or death: Nearly every state requires a report if an injury or death occurs, even if it’s minor.

- Property damage threshold: This is a specific dollar amount. If the damage to all vehicles and property in the accident exceeds this amount, a report is mandatory. These thresholds can be as low as $250 in Washington D.C., and as high as $3,000 in Hawai‘i and Vermont.

- Mandatory deadline: Once a report is required, the clock is ticking. The deadline to file with the state agency is highly inconsistent across the country. While many states demand reporting immediately or “as soon as possible,” others allow windows of five days, 10 days, or even up to six months.

CheapInsurance.com

The ‘Immediately’ Problem and Why the Police Report Isn’t Enough

Let’s talk frankly about that column labeled “Mandatory Deadline to State Agency.” You’ll notice a lot of entries that say “Immediately.”

“Immediately” in legal terms doesn’t mean “right after you finish your emergency room visit and call your mom.” It generally means “as soon as reasonably possible,” often within 24 to 48 hours. The point is this: don’t treat the state report as an afterthought. It’s a key administrative step.

Here’s the thing about the police: In many states, if the police show up and file an accident report, you still might be required to file your own report. Why? Because the police report focuses on fault and criminal/traffic violations. Your state report (often called an SR-1, SR-10, or similar) is an affidavit certifying your financial responsibility (insurance) and providing statistical data.

The Golden Rule: Never assume the police officer’s report covers your personal legal obligation to the state agency. Check your state’s specific form and requirement. When you see an “Immediately” deadline, make that report one of your top priorities once the dust has settled and you are safe. Ignore it, and you might find your driver’s license suspended, a penalty far worse than the accident itself.

The Consequences of an Unreported Accident to the DMV

Beyond the significant risk of an insurance claim denial, a private, unreported accident can expose you to direct legal penalties from the state. Your legal obligation to report an accident is distinct from your contractual obligation to your insurer. The consequences for failure to report an accident to the DMV vary by state.

The state’s requirement to file an official accident report (often with the Department of Motor Vehicles or State Police) is triggered not by whether a claim is filed, but by the severity of the incident itself. In most jurisdictions, an accident resulting in any injury or exceeding a statutory property damage threshold (which varies by state, but is commonly $1,000 to $2,000) must be reported.

Failure to file this legally required report is a violation of state motor vehicle law and can result in severe, non-negotiable penalties:

1. Driver’s License Suspension

The most immediate consequence of failing to comply with mandatory state reporting is the suspension of your driving privileges.

If the other party involved in the accident files their own official report, and the state determines that the incident met the mandatory reporting threshold, the state will investigate why your report is missing. Upon confirmation of the failure to report, the state will likely issue an order for the suspension or revocation of your driver’s license until you comply.

2. Avoid the Costly SR-22: Why Reporting Saves You Money

A driver’s license suspension for failing to comply with accident reporting rules frequently triggers a secondary and expensive requirement: the mandatory filing of an SR-22 Certificate of Financial Responsibility.

- What it is: An SR-22 is not an insurance policy itself, but a form filed by your insurance company with the state to certify that you carry the minimum required liability coverage. It is typically mandated for high-risk drivers (those with DUI convictions or multiple uninsured accidents).

- The financial burden: Being forced to obtain an SR-22 instantly places you into the high-risk insurance category. This requirement drastically increases your insurance rates for the mandated filing period, which is typically three to five years. The financial impact of the SR-22 requirement alone will almost certainly outweigh any perceived savings from attempting to handle the original fender bender privately.

3. Fines and Misdemeanor Charges

In many states, intentionally failing to file a legally required accident report is classified as a misdemeanor criminal offense. While less common, this can expose you to steep fines and, in extreme cases, potential jail time, depending on the severity of the unreported accident.

In short, while you may feel you are “getting away with it” by avoiding a phone call to your insurance agent, the consequences of failing to meet the state’s filing mandate are far more severe and are imposed directly by law, not by an insurance company contract. The state’s interest is in regulating financial responsibility, and a lack of reporting will be treated as an attempt to evade that responsibility.

CheapInsurance.com

Important Things to Remember

- This information is for guidance only: Laws change — always confirm the most current requirements with your state’s official DMV or law enforcement agency.

- The clock is ticking: Don’t delay. Many states have a tight deadline, often requiring you to file “immediately” or within a few days.

- When in doubt, report it: It’s always better to be safe than sorry. If you’re unsure whether your accident meets the reporting threshold, file the report anyway. It’s a simple step that could save you from potential legal issues down the road.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

![]()