Ranked: The cheapest and most expensive cars to insure in 2026. What’s driving the difference?

Tricky_Shark // Shutterstock

A new analysis of more than 3,000 vehicle models finds that the annual gap between the cheapest and most expensive cars to insure is around $4,400.

The analysis, conducted by CarInsurance.com, ranks vehicles from the most affordable to the most expensive to insure. The findings show a clear divide: Safe, affordable compact SUVs and crossovers are among the least expensive to insure, while luxury, high-performance models, especially BMW’s M-series, are among the most expensive.

Your car’s make and model play a major role in how much you pay for insurance because insurers use that information to estimate future claim costs. They look at past data for each vehicle, including repair expenses, theft rates and safety ratings.

In almost all cases, a vehicle’s overall risk profile matters just as much as its sticker price. Cars with strong safety ratings, lower repair costs and affordable parts are typically cheaper to insure and can help keep premiums in check. Understanding which vehicles carry lower premiums and why can help drivers make smarter purchasing decisions before they commit to a car. This CarInsurance.com analysis ranks vehicles from the most affordable to the most expensive to insure.

Still uncertain? An online car insurance calculator can help estimate how much you can expect to pay in your state.

Key findings: Cheapest and most expensive cars to insure

- The BMW M8 Gran Coupe ($6,744), BMW M5 Touring ($6,708) and BMW M5 ($6,593) are the most expensive vehicles to insure.

- Subaru Crosstrek ($2,299), Jeep Wrangler ($2,307) and Honda CR-V ($2,316) are the cheapest cars to insure in 2026, according to CarInsurance.com’s data study.

- Car insurance rates vary by make and model based on factors such as repair costs, safety ratings, theft rates, crash statistics and performance, all of which help insurers estimate the likelihood and cost of future claims.

- The cheapest cars to insure typically have high safety ratings, lower horsepower and low theft rates. Comparing insurance quotes before buying and choosing a slightly older model can further reduce premiums.

Cheapest cars to insure in 2026

Some models consistently have lower insurance rates due to favorable safety records and low repair costs.

These are the cheapest vehicles to insure and their average annual rates for full coverage car insurance:

- Subaru Crosstrek: $2,299

- Jeep Wrangler: $2,307

- Honda CR-V: $2,316

- Subaru Outback: $2,322

- Volkswagen Tiguan: $2,329

Most expensive cars to insure in 2026

Luxury and high-performance models often carry higher insurance premiums due to costly repairs and a higher theft risk.

These are the most expensive vehicles to insure and their average annual full-coverage rates:

- BMW M8 Gran Coupe: $6,744

- BMW M5 Touring: $6,708

- BMW M5: $6,593

- BMW M8: $6,423

- Audi e-tron GT: $6,413

These vehicles cost more to insure due to high-performance engines, expensive parts, higher theft rates and costly collision claims. The annual premiums for luxury and performance models often exceed $6,000.

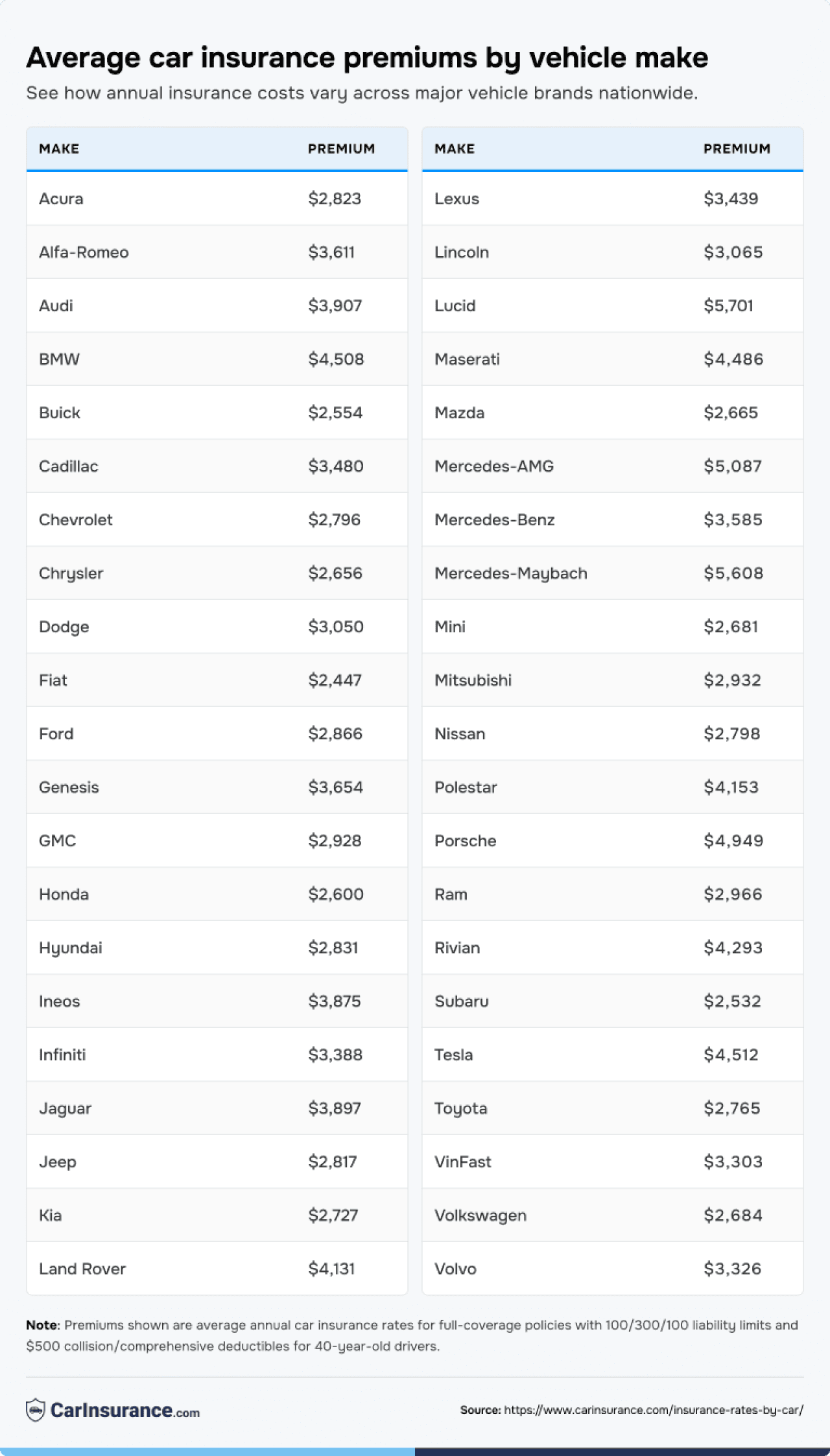

How much does insurance cost by vehicle make?

Insurance costs can also differ significantly by vehicle make. The table below shows average monthly premiums across all models for major vehicle makes, based on CarInsurance.com’s 2026 rate analysis.

CarInsurance.com

Brent Buell, lead data analyst at CarInsurance.com, said that trim level is an often-overlooked factor in premium pricing.

“Two versions of the same model can have very different insurance costs. A base-trim sedan and its high-performance variant may share a model name, but from an insurer’s perspective, they’re entirely different risk profiles,” Buell said. “The performance version has more horsepower, a higher MSRP and more expensive components to repair or replace.”

Why do insurance costs vary by vehicle?

The biggest factors insurers use to set rates are the type of vehicle, its repair or replacement costs and the driver’s risk profile.

Key factors that drive cost differences include:

- Repair costs: Luxury brands have expensive parts and labor.

- Safety ratings: Vehicles with advanced safety features often net lower rates.

- Theft rate: Frequently stolen vehicles typically cost more to insure.

- Crash stats: Cars involved in more severe accidents may carry higher risk loads.

- Performance: Sports cars are often rated as high-risk.

“There are many reasons why insurance rates vary from model to model and make to make,” said Brian Moody, senior editor at Autotrader. “The main consideration is the cost of repair. An insurance company has a responsibility to its customers and employees to make financially wise decisions. If an insured drives a Rolls-Royce, it’s logical that the cost will be higher for that customer because that specific car may be rare and expensive to repair. The expected availability of parts is also a factor.”

Here’s how it works in actuality

If a vehicle is worth $10,000, it would cost much less to insure than a vehicle worth $60,000, because the cost of parts is higher for a higher-value vehicle.

If a vehicle is totaled, replacing a $10,000 car versus a $60,000 car is a significant price difference, making insurance more expensive for newer, more expensive cars.

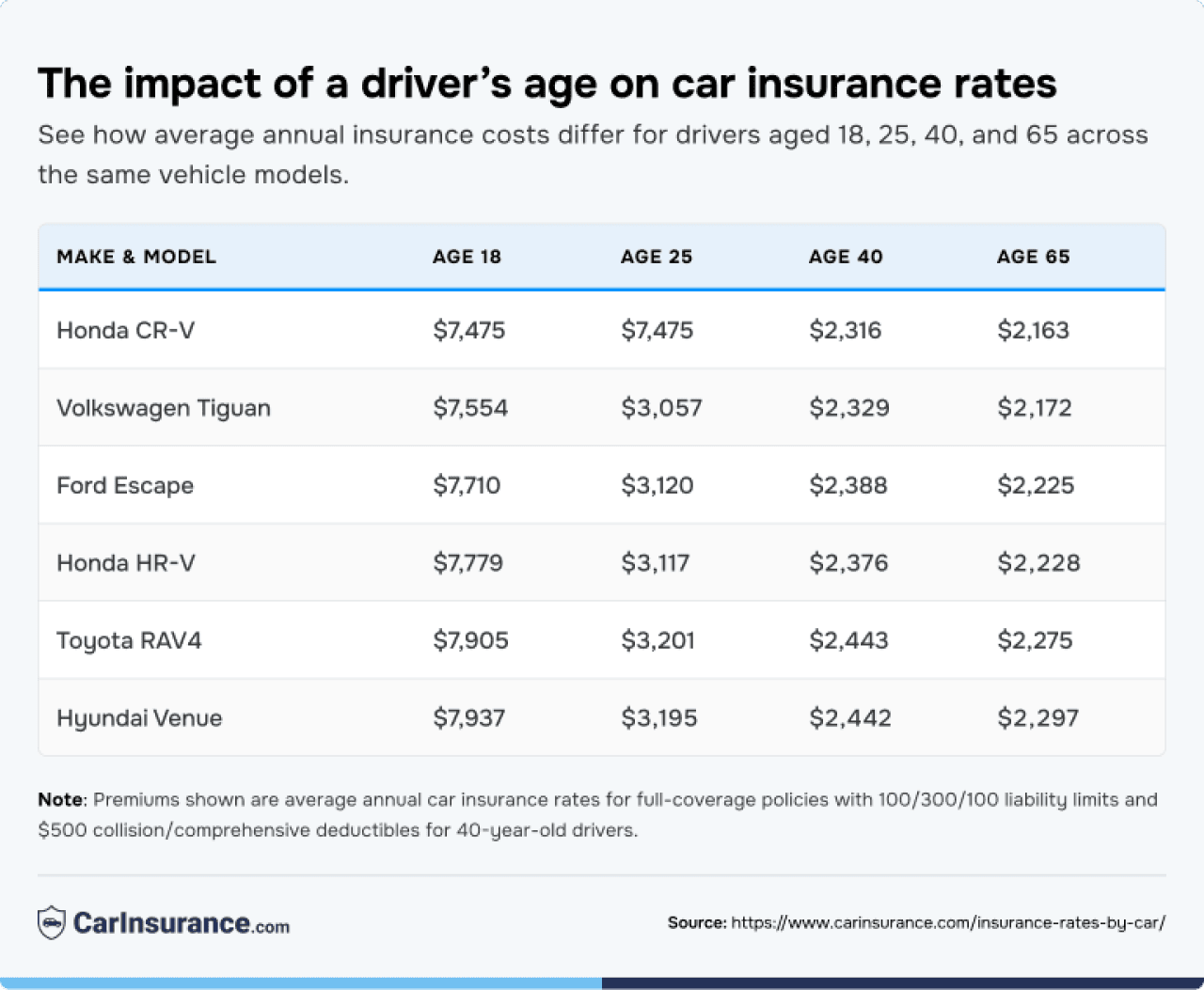

How does a driver’s age affect car insurance rates by make and model?

A driver’s age plays a major role in car insurance costs across all vehicles, with younger drivers paying the highest rates and middle-aged drivers the lowest. And the type of car you choose can increase the differences.

For example, an 18-year-old with a Ford Escape might pay $7,710 for insurance, while a 40-year-old with the same car would pay $2,388.

The table below shows how insurance premiums vary for the same cars depending on different drivers at ages 18, 25, 40 and 65.

CarInsurance.com

Choosing the first car for a teen

When buying a teen driver’s first car, focus on safe and reliable models. Vehicles with strong crash-test ratings and readily available parts tend to have lower insurance costs, even for younger drivers. Avoiding high-horsepower trims and luxury features can help keep premiums manageable as teens gain experience behind the wheel.

Insurance after retirement

If you are nearing or in retirement, picking the right car can help keep your insurance costs down as you get older. Cars with good safety ratings, fewer claims and lower repair costs often have the best rates for senior drivers. Switching to a practical, reliable car can lower your premiums without sacrificing comfort or safety.

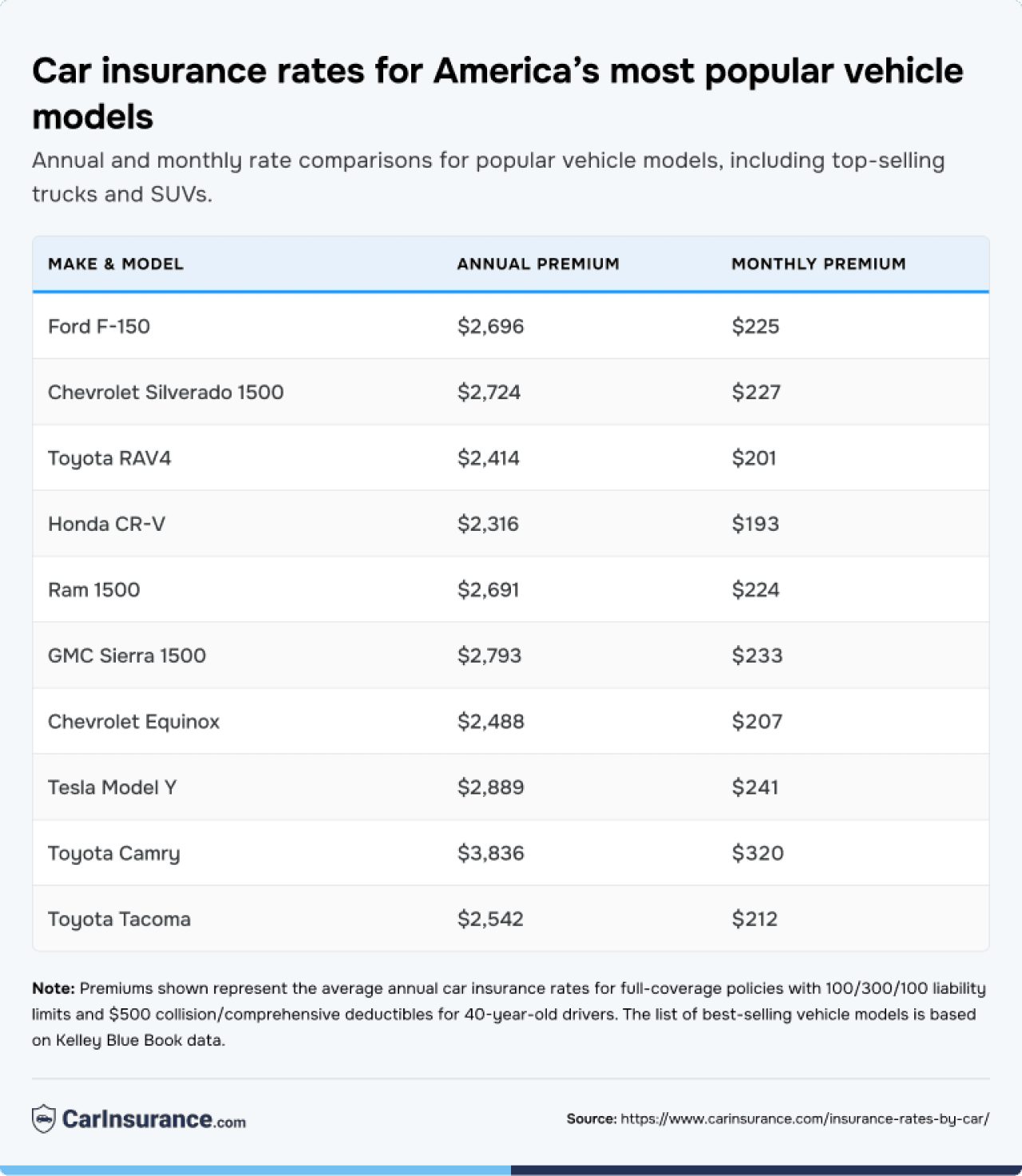

Insurance rates for America’s most popular car models

Below is a snapshot of estimated insurance costs for some of the best-selling vehicles in the U.S. — most of which are trucks — including the Ford F-150, Chevrolet Silverado, Ram 1500, GMC Sierra 1500 and Toyota Tacoma, among others.

CarInsurance.com

What is a car’s make and model?

Think of a car make and model like your last and first names. The “make” is the car’s last name or brand name — Dodge, Lexus, BMW, Tesla, etc. The “model” would be your first name — the individual model of the vehicle, so this would be Camry (Toyota), Ram (Dodge) or Fusion (Ford).

How to choose a car that’s cheaper to insure

- Choose models with high safety ratings (look at data from the IIHS or NHTSA).

- Avoid high-horsepower performance trims.

- Check theft history and loss data reports.

- Get insurance quotes before purchasing.

- Consider vehicle age — slightly older cars can be cheaper to insure and may not require full coverage.

“A high-horsepower car will cost more, as will a specialty car. Factoring that in before making a purchase can really help manage costs,” Moody said.

Chong Gao, director of product management, research and development at Mercury Insurance, agreed.

“Carefully compare quotes from different insurers on the various vehicles you are considering,” Gao said. “Luxury and high-performance vehicles tend to cost more to insure, as well as larger vehicles that have the potential to cause more damage.”

Additionally, if your vehicle is older, consider reducing your insurance coverage to liability only.

“As the actual cash value of your car drops, it could be more cost-effective to replace or repair the vehicle yourself in the event of an accident instead of paying for comprehensive and collision coverages,” Gao said.

How to use insurance rates by car to choose the right vehicle

The smartest way to avoid an unexpectedly expensive car that comes with high insurance rates is to compare quotes before you buy. Start with models you actually like, then use insurance data to narrow your choices.

Simplify your car search

1. Make a short list of three to five cars you’d genuinely be happy driving.

2. Use the insurance rates by make and model calculator to compare full-coverage premiums in your state.

3. Check age-based costs if the car is for a teen driver.

4. Get quotes from multiple insurers for your exact driver profile.

5. Adjust deductibles and coverage limits while maintaining adequate protection.

Use the insurance rates by make and model calculator to narrow your options, then shop around and compare coverage details to make the final choice that fits your budget.

Key takeaways: How car choice impacts insurance costs

The more expensive your car is, the more you’ll pay for car insurance. If cost is your main concern when shopping for a vehicle, make sure you buy a car that’s highly rated for safety, is not frequently stolen and is one of the cheapest cars to insure.

Frequently Asked Questions:

Which type of car is usually cheapest to insure?

Midsize SUVs with high safety scores and low repair costs typically have the lowest premiums.

Do newer cars cost more to insure?

Not always. New cars with good safety features may qualify for discounts, but they can cost more to repair.

Why do sports cars cost more to insure?

Sports cars are driven faster, have higher accident rates and cost more to repair, raising insurance costs.

How can I check insurance costs before buying a car?

Use an online tool to get a car insurance estimate by model using your vehicle’s make, model and year.

Does the car’s value affect insurance rates?

Yes. Higher value often means more expensive repairs and payouts, increasing premiums.

Can a car’s trim and body style affect your car insurance rates?

Yes. Pricier trim levels that offer greater horsepower and luxury features can increase the vehicle’s MSRP, raising rates.

How do safety ratings affect insurance rates?

Safety ratings reflect how well the vehicle protects its occupants in a crash. This will be reflected in your personal injury protection/medical payments coverage, but it is only a small portion of the total cost.

Does the color of your car affect car insurance premiums?

No, the color of your vehicle is not a rating factor for determining the cost of your policy.

Methodology

CarInsurance.com conducted a comprehensive analysis using billions of data points to provide accurate, insightful information on how the type of car you drive affects auto insurance premiums.

To ensure consistency, calculations were based on the sample driver profile of a 40-year-old male driver (unless otherwise stated) carrying a full coverage policy with limits of 100/300/100 and $500 collision/comprehensive deductibles. The driver has a 12-mile commute, an annual mileage of 10,000 miles and maintains a clean driving record with no accidents or violations.

This story was produced by CarInsurance.com and reviewed and distributed by Stacker.

![]()